The Dutch tax on a house in Spain is calculated within box 3, but thanks to the international tax treaty, you do not actually have to pay tax in the Netherlands on this property. Although you are required to report the value of the Spanish property in your annual tax return, the Inland Revenue grants a deduction to avoid double taxation. This shifts the effective tax burden entirely to the Spanish tax authorities. This mechanism is crucial for property owners to avoid double taxation on their holiday home.

Understanding the Dutch taxes on houses in Spain is essential for any property owner.

However, keep in mind the capital gains tax and the specific tax implications for your total assets in the Netherlands.

- Exemption through the applicable tax treaty.

- Reporting in Box 3 always remains mandatory.

- Specific deduction effectively prevents double taxation.

- Dutch tax on a house in Spain often remains nil.

How does Dutch tax on a house in Spain work?

Owning a second home under the Spanish sun is a dream come true for many Dutch people. However, once the purchase deed is signed and the keys handed over, you will have to deal with complex tax regulations that extend across national borders. Dutch tax on a house in Spain is a subject that often causes confusion, as you have to deal with the laws of two different countries.

Basically, as a resident of the Netherlands, you are required to declare your worldwide assets to the tax authorities. This means that your Spanish villa, flat or village house is simply part of your taxable base in box 3. Although the property is physically abroad, the tax authorities in the Netherlands look at the value of this asset to determine how much capital gains tax you theoretically owe on your total capital.

Many owners wonder if they are being taxed twice, as Spain also claims to tax property on their territory.

Fortunately, the Netherlands and Spain have concluded a tax treaty to avoid paying the full amount of tax twice on the same property. This treaty stipulates that the country where the property is located, in this case Spain, has the primary right to levy tax. However, this does not alter the fact that you still have to declare the property in your Dutch income tax return.

The Tax rules for a Spanish property provide that you get a so-called ‘double tax relief’ in the Netherlands. This significantly reduces the effective pressure of Dutch tax on a house in Spain, but the value of the house still counts when determining the amount of your total wealth and any tax-free wealth thresholds.

To the value of your property in Spain correctly, you have to use the market value. In the Netherlands, we are familiar with the WOZ value, but for foreign properties, you have to make your own realistic estimate of the sales value in unoccupied state on the reference date of 1 January. It is essential to be precise when doing this, as the tax authorities may carry out checks on the amounts provided.

In practice, many people use the purchase price or a recent valuation as the starting point for their tax return. Understanding the Calculating Dutch tax on a house in Spain for individuals is crucial to avoid unpleasant surprises at the final assessment, especially now that the rules surrounding box 3 have been in considerable flux in recent years due to various court rulings.

The role of box 3 and the tax treaty

Within the Dutch tax system, a second home is not in box 1 (work and home), but in box 3 (savings and investments). This means that any actual rental income you may receive from the home in Spain is not directly taxed in the Netherlands. Instead, the tax authorities levy on a flat rate return based on the value of the property minus any debts, such as a mortgage taken out specifically for that property.

The calculation of the capital gains tax has recently become more complex due to the distinction between bank deposits and other assets. Because a house in Spain is considered an ‘other property’, a higher flat rate of return is calculated than for savings. This makes it all the more important to apply deductions correctly.

“Avoiding double taxation is a right derived from international treaties, but the burden of proof for the correct valuation of foreign property always lies with the taxpayer himself.”

When you file a tax return, the Inland Revenue programme first calculates the tax on your entire worldwide assets. It then applies a proportional reduction for the part related to your Spanish home. This process ensures that the Dutch tax on a house in Spain often amounts to a nil return in terms of actual payment, provided the calculation is done correctly.

Nevertheless, home ownership may affect other schemes, such as the amount of certain allowances or the general tax credit, as your aggregate income may increase due to the notional return in Box 3. It is therefore advisable to always keep a current overview of the market value and associated debts.

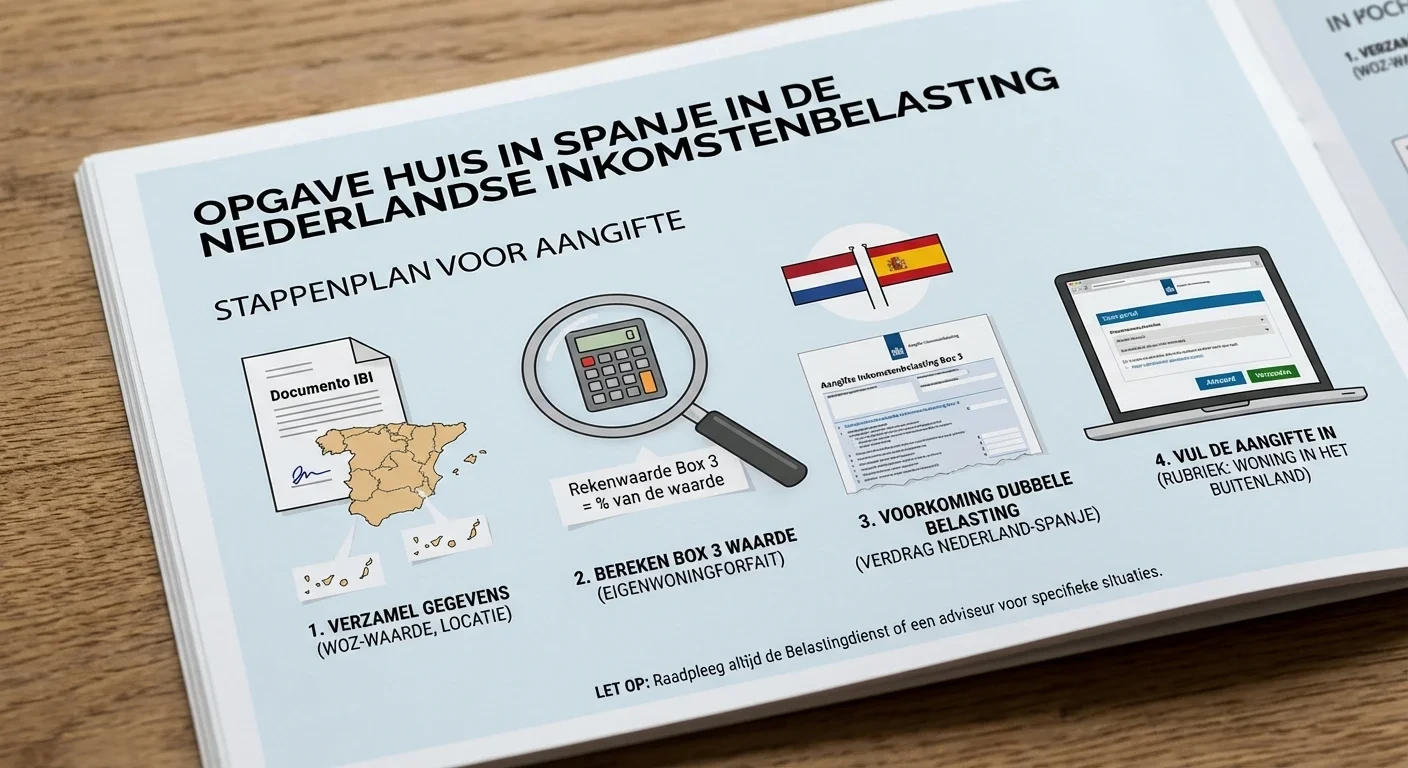

Main steps for your declaration (NL)

- Determine which category it falls into

- Does it involve a second home (holiday/investment)? Then this usually belongs to box 3.

- Are you going to live permanently yourself (main residence)? If so, the treatment may be different; if in doubt, have a tax check.

- Determine value according to the Inland Revenue rule for foreign property

For a property abroad, use the fair value (market value) in uninhabited and unrented state at 1 January of the year preceding the year of declaration.

Practical evidence: valuation report, recent comparable sales, purchase price (corrected), broker's valuation. - Note your ownership percentage

Do you own alone or together (with partner/family)? Please indicate your share on. - Map debts associated with the property

Think of a mortgage or loan you took out for purchase/renovation. (That usually also belongs in box 3.) - Complete your box 3 tax return

You list the property as (foreign) property / 2nd home by land Spain and the value according to step 2. - Check double tax relief

Because Spain is allowed to levy on Spanish property, you are basically entitled to a double taxation relief (via treaty or arrangement).

Note that depending on your total assets, it may still feel like you are paying “something” in NL; so check carefully what the tax return calculates. - Save your substantiation

Save valuation/appraisal, purchase deed, mortgage statement and any Spanish assessments neatly for any questions afterwards.

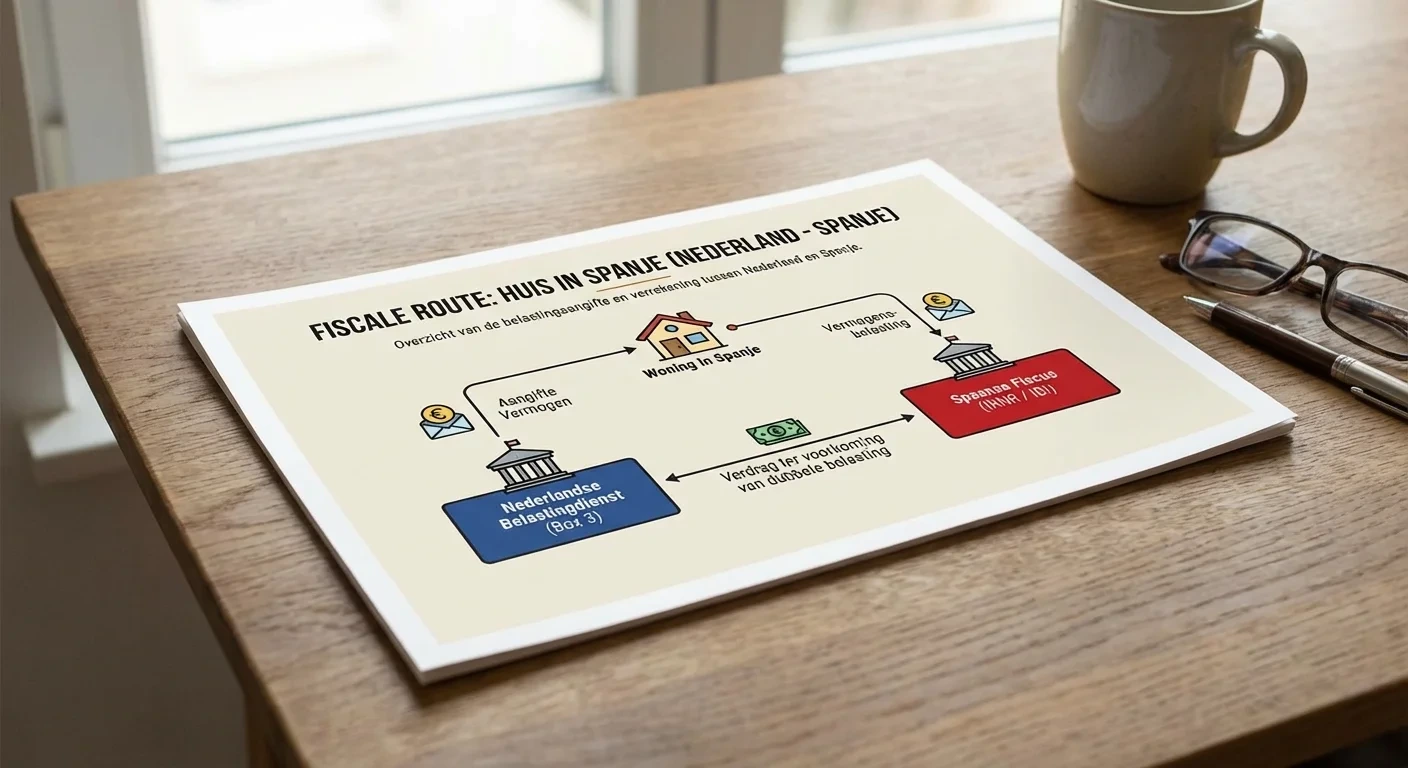

Box 3 and avoiding double taxation

When you own a second home across the border as a resident of the Netherlands, you inevitably face complex tax rules. Dutch tax on a house in Spain is initially calculated in Box 3, where your worldwide assets are taxed. However, as Spain also has the right to tax property on their territory, a risk of double taxation arises. To avoid this, the two countries have signed a tax treaty. This treaty ensures that you do not pay the full amount twice, but that the Netherlands grants a reduction on the tax to be paid. In practice, this means that the value of the Spanish home does count when determining your total assets, but then a deduction is made to avoid double taxation.

The calculation of this deduction is based on the ratio of your foreign assets to your total worldwide assets in Box 3.

The tax treaty between the Netherlands and Spain

The current treaty is essential for anyone who wants to understand Dutch tax on a house in Spain. The Netherlands applies the so-called exemption method with progression proviso. This means that the value of your Spanish property is included in the yield basis, but the tax you would owe on it is immediately deducted from the total again. As a result, you effectively only pay tax in Spain on the property itself, while in the Netherlands it can only affect the rate applicable to your other assets. It is crucial to note that you Tax rules for Dutch taxation of property abroad correctly applied in your annual tax return to avoid fines or additional taxes.

“Avoiding double taxation is a fundamental right for cross-border property owners within the European Union.”

For more detailed information on international treaties, please visit the website of the Inland Revenue consult for current regulations.

Important points of attention for the tax return

- Always declare the current market value of the property in Box 3.

- Don't forget to explicitly request the double tax deduction.

- Take into account any debts directly related to the property.

Important tax obligations for your Spanish property

When you own property abroad, you will inevitably face complex regulations in both the country of origin and the country of residence. For many owners, the Dutch tax on a house in Spain is an issue during the annual tax return to the tax authorities. Although the property is physically located in Spain, you have to declare its value in Box 3 as part of your worldwide assets. However, this does not mean that you will be directly double taxed, as international treaties exist to prevent this. It is essential to accurately report the current WOZ value or Spanish market value to avoid penalties.

Preventing double taxation

Fortunately, the tax treaty between the Netherlands and Spain provides for an arrangement whereby you get a reduction to avoid double Dutch tax on a house in Spain for individuals.

In practice, this works through the so-called exemption method, where the tax authorities calculate what part of your assets are abroad. You effectively pay less tax on your total assets in the Netherlands because the right to tax the property lies primarily with the Spanish government. Nevertheless, the declaration of Dutch tax on a house in Spain remains mandatory for every resident. Failure to declare these assets correctly can lead to retrospective assessments and significant increases in the amounts owed by the tax authorities.

Local Spanish taxes versus Box 3

“Understanding the interaction between local IBI and the Dutch capital gains tax is crucial for sound financial planning of your holiday home.”

In addition to the Dutch tax on a house in Spain, you need to consider locally the Impuesto sobre Bienes Inmuebles (IBI) and the non-resident tax. For more detailed information on international treaties, visit the Tax Office website for up-to-date guidelines. Dutch tax on a house in Spain declaration in box 3 requires precision and knowledge of the latest legislative changes.

Therefore, always make sure you have the right documentation, such as the purchase deed and local tax assessments. Good preparation for the Dutch tax on a house in Spain obligations saves you a lot of worry and unnecessary costs in the long run.

- Check the value date for Box 3 annually.

- Request the Spanish Valor Catastral in good time.

Understanding Dutch tax on a house in Spain is essential for any property owner.

Although you pay local taxes in Spain, you must also report the property in box 3 of your Dutch tax return. Fortunately, the tax treaty between the two countries prevents double taxation through a double tax deduction.

In short, you are obliged to report the value of your Spanish home, but the actual financial burden in the Netherlands is often limited by international agreements. However, it is always advisable to consult a specialist for your specific situation, as legislation around capital gains tax changes regularly. Would you like to know more about the tax benefits or help with your declaration? Contact our advisers today for hassle-free handling of your Foreign assets and avoid unnecessary fines of the Inland Revenue.

Do I have to declare a property in Spain in my Dutch tax return?

Yes. If you are a taxpayer in the Netherlands, you must include your foreign assets (such as a property in Spain) in your tax return. In most cases, this is box 3 (e.g. a holiday or investment home).

Is my property in Spain in box 1 or box 3?

A property in Spain generally falls into box 3 if it is a second home (holiday or investment). Only in specific situations (e.g. when treated as an own home/main residence) can box 1 come into the picture. If in doubt, a quick check with a tax expert is wise.

Which value should I use: WOZ or market value?

For foreign property, you do not use a WOZ value in the Netherlands. You usually report the market value (fair market value), often as if the property were unoccupied and unrented.

Which reference date applies to the value?

For box 3, the reference date of 1 January applies in principle. You determine the value of the property on that date of the relevant tax year.

What if I rent out the property (partly) in Spain?

Even then, you usually have to include the property in your Dutch tax return. Letting may additionally have tax consequences in Spain. In the Netherlands, it usually remains box 3, but details may differ from one situation to another.

Can I take the mortgage or loan for the property in Spain with me?

Debts belonging to Box 3 (such as financing for a second home) can reduce your Box 3 basis. Note the outstanding amount on the reference date and keep supporting documents.

Do I pay tax in both Spain and the Netherlands?

Spain is usually allowed to tax property located in Spain. The Netherlands usually avoids double taxation through a double tax relief. As a result, you usually do not pay ‘full double’, but the outcome depends on your total assets and situation.

Do I also have to declare in Spain as a non-resident?

Often it does. Spain has local levies (such as IBI) and in many cases rules for non-residents around (fictitious) income or rental income. This is separate from your Dutch tax return.

What documents should I keep as substantiation?

Preferably keep an appraisal/valuation or similar substantiation, the purchase deed, proof of renovations, and mortgage or loan statements. This will help with questions about the chosen value.

Where can I find the official rules?

The most reliable explanations can be found at the Tax Office (box 3 and foreign assets) and in information on the tax treaty with Spain. In case of doubt or complex situations, it pays to seek advice.

Service & Contact

Location: Alicante, Spain

Scope of work: Worldwide, Europe, Belgium, Netherlands, Germany, France

Services: Tax scan Spanish real estate, Box 3 optimisation advice, Double tax avoidance check, Wealth reporting Netherlands-Spain, Inheritance planning for second homes, Tax structuring in case of purchase, Audit of cross-border taxation

Target audience: Dutch pensioners with second residence in Spain, Property investors expanding their portfolio to the Spanish coast, Dutch expats in Belgium who remain fiscally connected to the Netherlands, High net worth individuals (HNWI) looking for tax optimisation, Families from the Netherlands considering a holiday home in Spain, Self-employed entrepreneurs (ZZP'ers) working remotely from a Spanish home, Heirs who have inherited a house in Spain from Dutch parents, Tax advisers and accountants specialising in international law, Dutch investors in holiday rentals in Spain